In a new weekly update for pv magazine, OPIS, a Dow Jones company, provides a quick look at the main price trends in the global PV industry.

OPIS

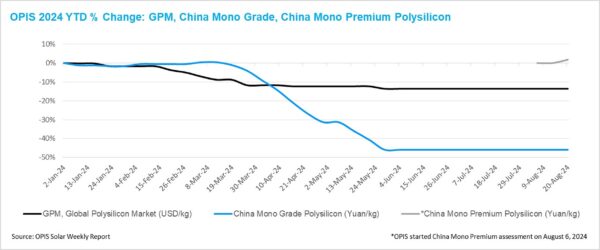

The Global Polysilicon Marker (GPM), the OPIS benchmark for polysilicon outside China, was assessed at $22.567/kg this week. This is unchanged from the previous week, as the fundamentals of this market segment remain largely stable for now.

Wafer plants in Southeast Asia have reportedly ramped up their operations recently, with the purpose to redirect these wafers to countries in the region outside the four countries currently under U.S. investigation, where they are processed into cells and modules intended for sale in the U.S. market.

This trend hasn’t led to changes in global polysilicon transaction prices. A Southeast Asian wafer producer mentioned preferring to buy polysilicon from traceable regions in China to reduce costs. Additionally, current global polysilicon inventories, built up from a sluggish spot market, are adequate to meet the slight increase in demand resulting from higher wafer production rates in Southeast Asia.

The fire triggered by a pipe explosion at a global polysilicon factory last week has drawn significant attention in the market. However, market participants agree that the incident will have a limited impact on the factory’s production capacity and is unlikely to affect global polysilicon prices.

This is partly because the manufacturer holds excess inventory after a customer postponed some regular monthly orders under a long-term purchase agreement, according to a market source. Additionally, with ongoing uncertainty around U.S. investigations into imported cells and modules from four Southeast Asian countries, global polysilicon demand remains subdued, further minimizing the potential impact on prices.

China Mono Grade, OPIS’ assessment for mono-grade polysilicon prices, held steady at CNY 33 ($4.62)/kg this week, marking twelve consecutive weeks of stability. Meanwhile, China Mono Premium, OPIS’ price assessment for mono-grade polysilicon used in N-type ingot pulling, rose by 1.79% from last week, reaching CNY 39.7 ($5.56)/kg.

The increase in prices of polysilicon used in N-type ingot pulling is attributed partly to a few wafer factories restocking their polysilicon inventory after depletion, and partly to futures and spot traders accumulating polysilicon in preparation of its potential listing as a futures commodity.

Major polysilicon giants, with their cost advantages and control over much of the market’s inventory, are increasingly demonstrating strong pricing power in the Chinese market. As smaller companies produce at limited operating rates, their regular customers are now turning to these major factories for spot purchases, further strengthening the giants’ influence on prices.

With the dry season approaching in two months in Sichuan and Yunnan – regions reliant on hydroelectric power and home to many polysilicon factories – rising electricity costs are expected to push up production costs. This will likely make it even harder for smaller, shuttered polysilicon enterprises to resume operations, thereby amplifying the pricing power of the major producers.

A market observer suggested that polysilicon giants may continue to raise prices, potentially reaching around CNY 50 ($7.01)/kg, slightly above their production costs. However, this level remains well below the cost threshold for smaller producers and is unlikely to spur the reopening of closed small factories.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Popular content

{kind=link}